Cash management services provider Brink's (NYSE:BCO) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 3.8% year on year to $1.30 billion. Guidance for next quarter’s revenue was better than expected at $1.33 billion at the midpoint, 2% above analysts’ estimates. Its non-GAAP profit of $1.79 per share was 23.7% above analysts’ consensus estimates.

Is now the time to buy Brink's? Find out by accessing our full research report, it’s free.

Brink's (BCO) Q2 CY2025 Highlights:

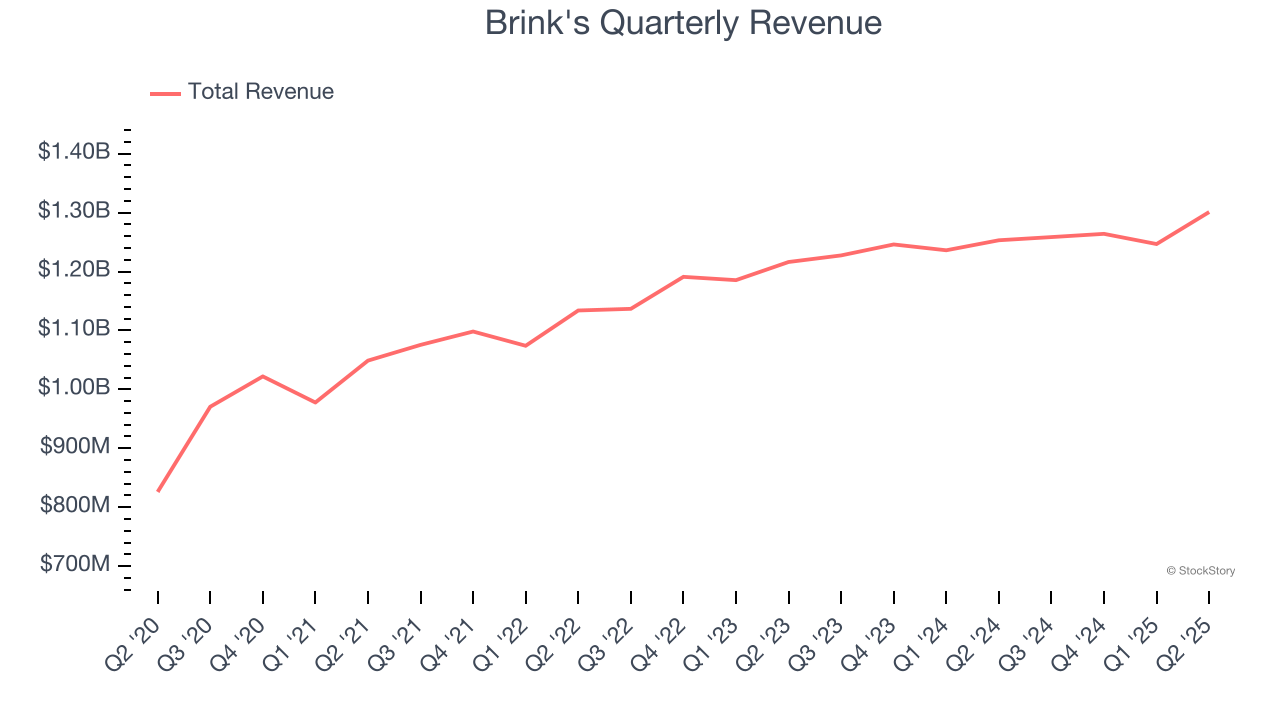

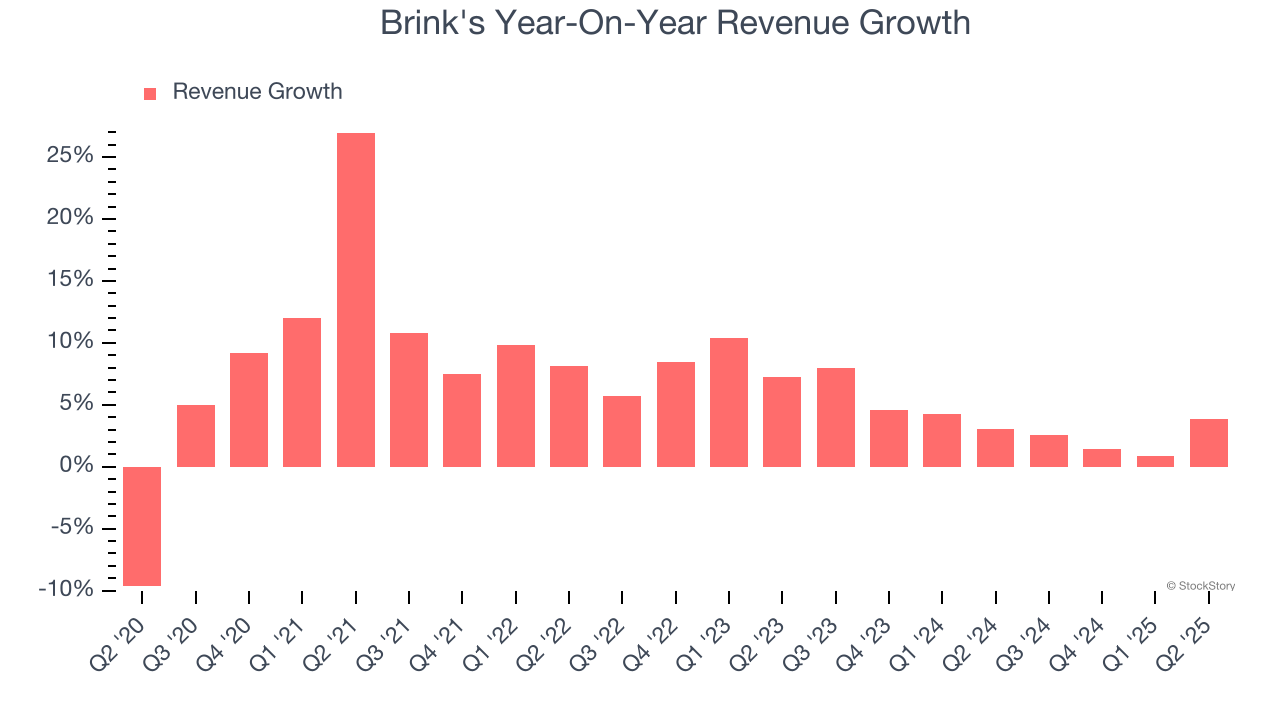

- Revenue: $1.30 billion vs analyst estimates of $1.27 billion (3.8% year-on-year growth, 2.1% beat)

- Adjusted EPS: $1.79 vs analyst estimates of $1.45 (23.7% beat)

- Adjusted EBITDA: $232 million vs analyst estimates of $215.9 million (17.8% margin, 7.5% beat)

- Revenue Guidance for Q3 CY2025 is $1.33 billion at the midpoint, above analyst estimates of $1.30 billion

- Adjusted EPS guidance for Q3 CY2025 is $2.05 at the midpoint, above analyst estimates of $2.01

- EBITDA guidance for Q3 CY2025 is $250 million at the midpoint, above analyst estimates of $244.8 million

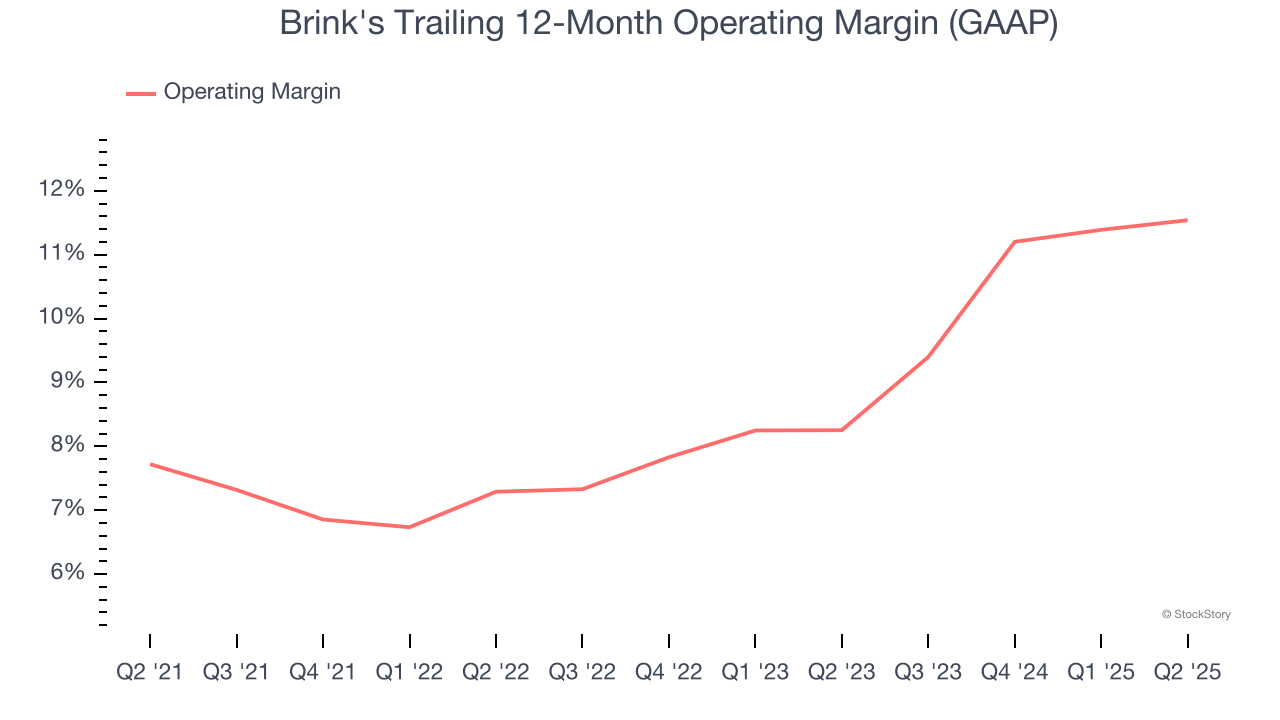

- Operating Margin: 10.3%, in line with the same quarter last year

- Free Cash Flow was $152.2 million, up from -$122.8 million in the same quarter last year

- Market Capitalization: $3.72 billion

Mark Eubanks, president and CEO, said: “I am proud of our consistent execution and the delivery of another quarter of meaningful progress against our strategic priorities. We continue to grow higher-margin subscription-based AMS / DRS revenue, expand our profit margins, improve our cash conversion and return capital to shareholders. This was clear in our strong second quarter performance which exceeded the top end of our quarterly guidance for revenue, EBITDA and EPS. We are increasing our expectations for the full-year, supported by strong operational momentum in the first-half of the year, good second-half visibility into accelerating AMS / DRS organic revenue growth, and favorable first-half currency trends."

Company Overview

Known for its iconic armored trucks that have been a fixture in American cities since 1859, Brink's (NYSE:BCO) provides secure transportation and management of cash and valuables for banks, retailers, and other businesses worldwide.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $5.07 billion in revenue over the past 12 months, Brink's is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Brink's grew its sales at a solid 7.3% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Brink’s recent performance shows its demand has slowed as its annualized revenue growth of 3.5% over the last two years was below its five-year trend.

This quarter, Brink's reported modest year-on-year revenue growth of 3.8% but beat Wall Street’s estimates by 2.1%. Company management is currently guiding for a 5.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Brink's was profitable over the last five years but held back by its large cost base. Its average operating margin of 9% was weak for a business services business.

On the plus side, Brink’s operating margin rose by 3.8 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q2, Brink's generated an operating margin profit margin of 10.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

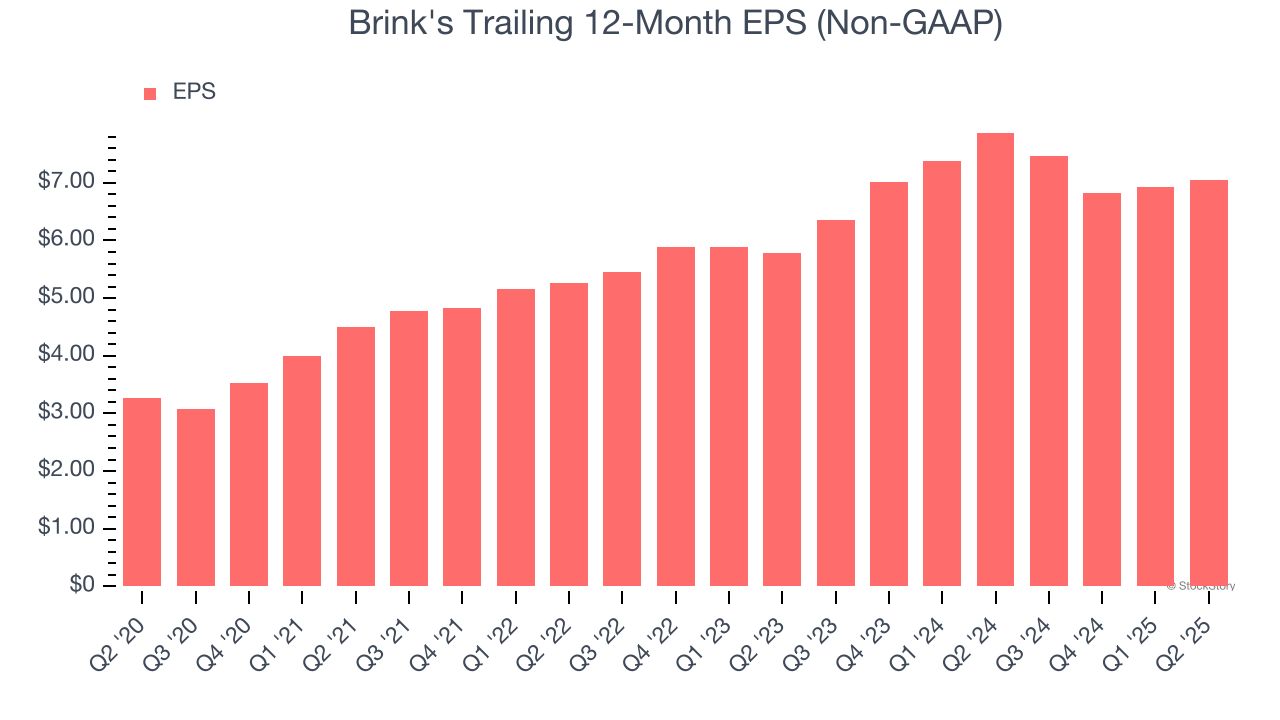

Brink’s EPS grew at an astounding 16.6% compounded annual growth rate over the last five years, higher than its 7.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

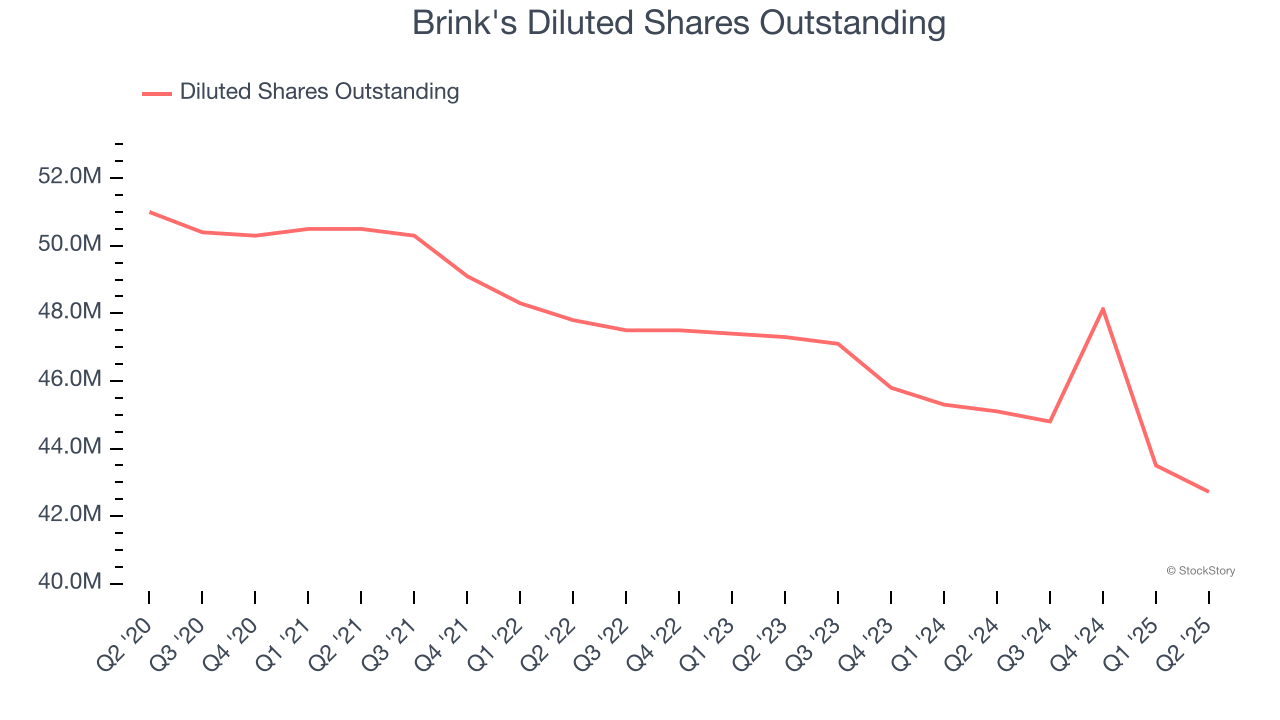

Diving into the nuances of Brink’s earnings can give us a better understanding of its performance. As we mentioned earlier, Brink’s operating margin was flat this quarter but expanded by 3.8 percentage points over the last five years. On top of that, its share count shrank by 16.2%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Brink's, its two-year annual EPS growth of 10.4% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q2, Brink's reported adjusted EPS at $1.79, up from $1.67 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Brink’s full-year EPS of $7.04 to grow 14.1%.

Key Takeaways from Brink’s Q2 Results

We were impressed by how significantly Brink's blew past analysts’ EPS expectations this quarter. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 2.6% to $91 immediately following the results.

Brink's put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.