Let’s dig into the relative performance of Integer Holdings (NYSE:ITGR) and its peers as we unravel the now-completed Q4 medical devices & supplies - specialty earnings season.

The medical devices industry operates a business model that balances steady demand with significant investments in innovation and regulatory compliance. The industry benefits from recurring revenue streams tied to consumables, maintenance services, and incremental upgrades to the latest technologies, although specialty devices are more niche. The capital-intensive nature of product development, coupled with lengthy regulatory pathways and the need for clinical validation, can weigh on profitability and timelines. In addition, there are constant pricing pressures from healthcare systems and insurers maximizing cost efficiency. Over the next several years, one tailwind is demographic–aging populations means rising chronic disease rates that drive greater demand for medical interventions and monitoring solutions. Advances in digital health, such as remote patient monitoring and smart devices, are also expected to unlock new demand by shortening upgrade cycles. On the other hand, the industry faces headwinds from pricing and reimbursement pressures as healthcare providers increasingly adopt value-based care models. Additionally, the integration of cybersecurity for connected devices adds further risk and complexity for device manufacturers.

The 6 medical devices & supplies - specialty stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 0.8%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 25.2% since the latest earnings results.

Integer Holdings (NYSE:ITGR)

With its name reflecting the mathematical term for "whole" or "complete," Integer Holdings (NYSE:ITGR) is a medical device outsource manufacturer that produces components and systems for cardiac, vascular, neurological, and other medical applications.

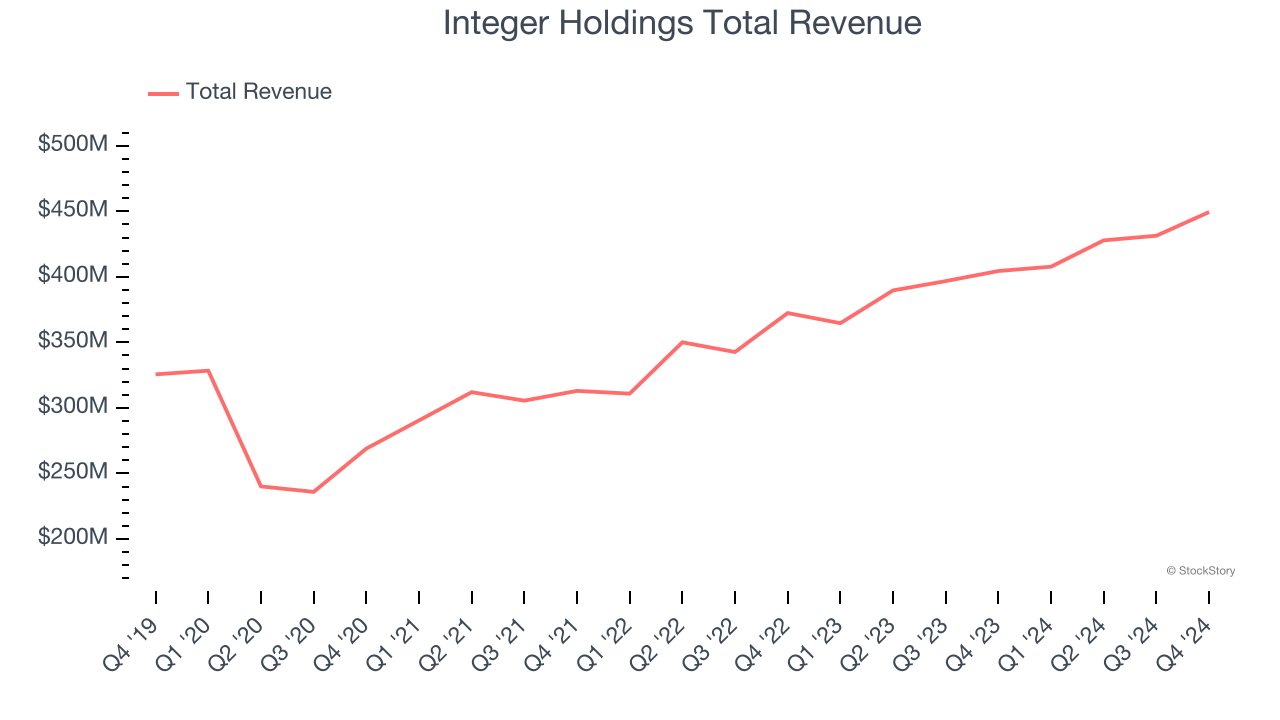

Integer Holdings reported revenues of $449.5 million, up 11.1% year on year. This print exceeded analysts’ expectations by 0.6%. Despite the top-line beat, it was still a mixed quarter for the company with full-year revenue guidance slightly topping analysts’ expectations but a miss of analysts’ EPS estimates.

“Integer delivered strong fourth quarter and full year 2024 sales and income with full year sales up 10% and adjusted operating income up 20%,” said Joseph Dziedzic, Integer’s president and CEO.

Integer Holdings scored the highest full-year guidance raise of the whole group. Still, the market seems discontent with the results. The stock is down 22.4% since reporting and currently trades at $107.30.

Is now the time to buy Integer Holdings? Access our full analysis of the earnings results here, it’s free.

Best Q4: Inspire Medical Systems (NYSE:INSP)

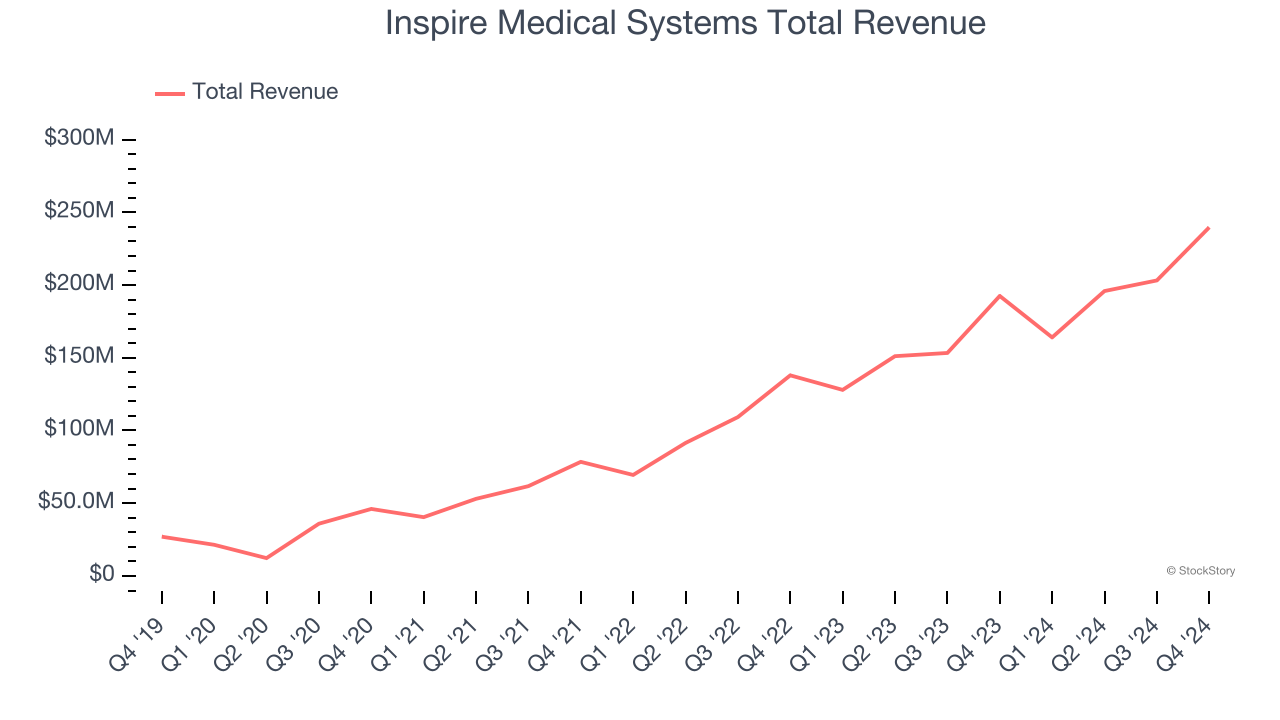

Offering an alternative for the millions who struggle with traditional CPAP machines, Inspire Medical Systems (NYSE:INSP) develops and sells an implantable neurostimulation device that treats obstructive sleep apnea by stimulating nerves to keep airways open during sleep.

Inspire Medical Systems reported revenues of $239.7 million, up 24.5% year on year, outperforming analysts’ expectations by 0.9%. The business had a very strong quarter with an impressive beat of analysts’ EPS estimates.

Inspire Medical Systems pulled off the fastest revenue growth among its peers. The stock is down 22.4% since reporting. It currently trades at $140.41.

Is now the time to buy Inspire Medical Systems? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Haemonetics (NYSE:HAE)

With roots dating back to 1971 and a mission to improve blood-related healthcare, Haemonetics (NYSE:HAE) provides specialized medical devices and software for blood collection, processing, and management across plasma centers, blood banks, and hospitals.

Haemonetics reported revenues of $348.5 million, up 3.7% year on year, falling short of analysts’ expectations by 1.3%. It was a slower quarter as it posted organic revenue in line with analysts’ estimates.

Haemonetics delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 20.7% since the results and currently trades at $56.48.

Read our full analysis of Haemonetics’s results here.

Globus Medical (NYSE:GMED)

With operations spanning 64 countries and a portfolio of over 10 new products launched in 2023 alone, Globus Medical (NYSE:GMED) develops and sells implantable devices, surgical instruments, and technology solutions for spine, orthopedic, and neurosurgical procedures.

Globus Medical reported revenues of $657.3 million, up 6.6% year on year. This result surpassed analysts’ expectations by 1.9%. Overall, it was a strong quarter as it also produced a solid beat of analysts’ EPS estimates and a narrow beat of analysts’ constant currency revenue estimates.

Globus Medical pulled off the biggest analyst estimates beat among its peers. The stock is down 20% since reporting and currently trades at $67.27.

Read our full, actionable report on Globus Medical here, it’s free.

Enovis (NYSE:ENOV)

With a focus on helping patients regain or maintain their natural motion, Enovis (NYSE:ENOV) develops and manufactures medical devices for orthopedic care, from injury prevention and pain management to joint replacement and rehabilitation.

Enovis reported revenues of $561 million, up 23.3% year on year. This print beat analysts’ expectations by 1%. Taking a step back, it was a mixed quarter as it also recorded a decent beat of analysts’ EPS estimates but full-year revenue guidance slightly missing analysts’ expectations.

The stock is down 36.4% since reporting and currently trades at $26.77.

Read our full, actionable report on Enovis here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.