Etsy trades at $43.06 per share and has moved almost in lockstep with the market over the last six months. The stock has lost 13.3% while the S&P 500 is down 9.8%. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Etsy, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Even though the stock has become cheaper, we're cautious about Etsy. Here are three reasons why ETSY doesn't excite us and a stock we'd rather own.

Why Is Etsy Not Exciting?

Founded by a struggling amateur furniture maker Robert Kalin and his two friends, Etsy (NASDAQ:ETSY) is one of the world’s largest online marketplaces, focusing on handmade or vintage items.

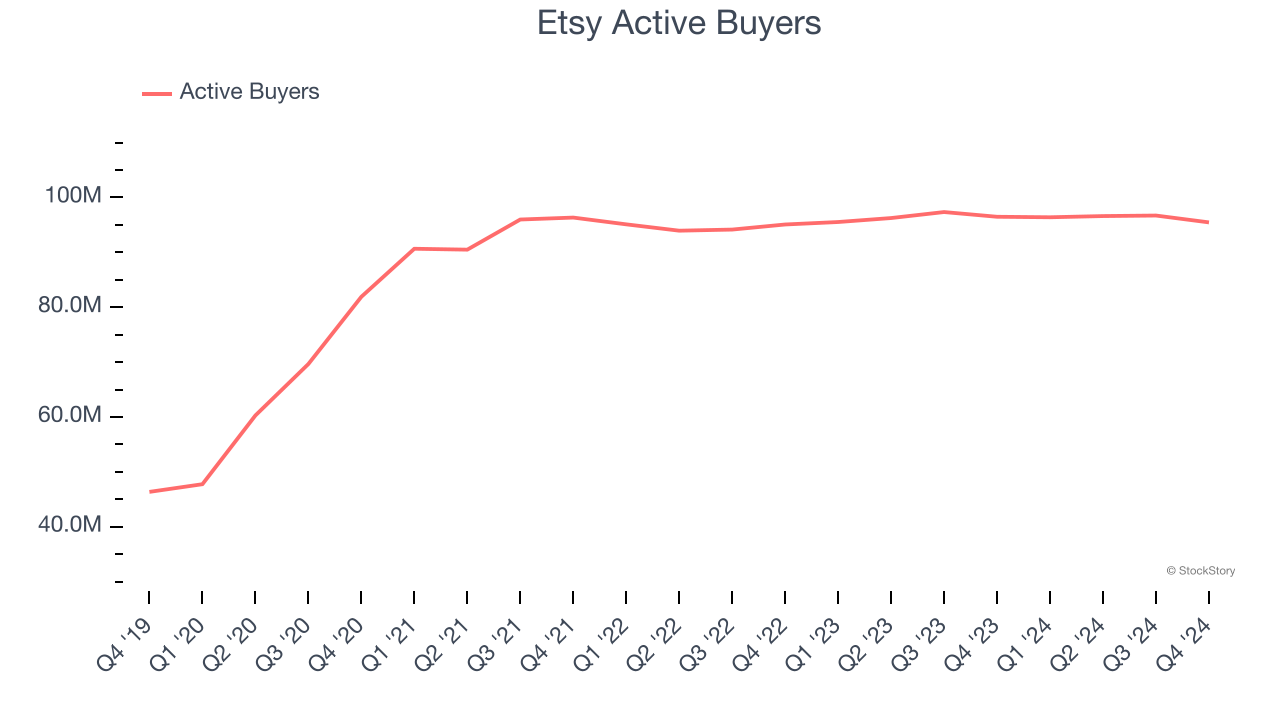

1. Active Buyers Hit a Plateau

As an online marketplace, Etsy generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Etsy struggled with new customer acquisition over the last two years as its active buyers were flat at 95.46 million. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Etsy wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Etsy’s revenue to stall, a deceleration versus its 6.4% annualized growth for the past three years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

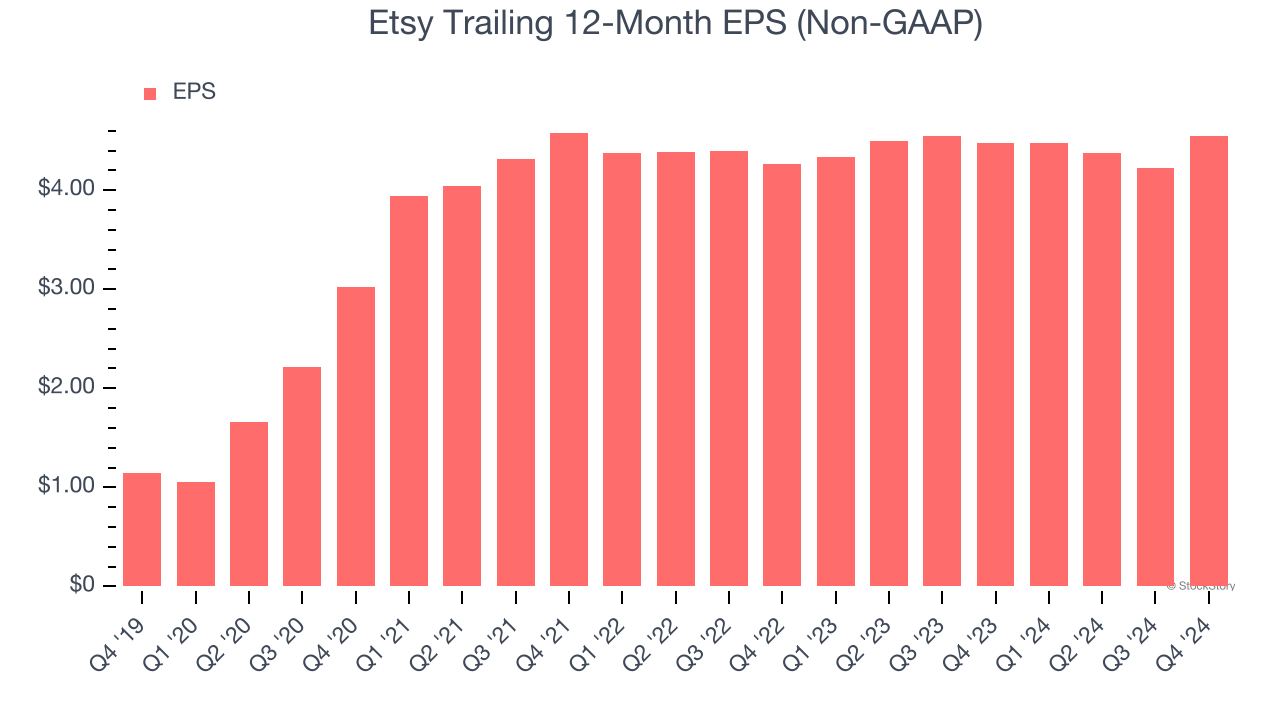

3. EPS Growth Has Stalled

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Etsy’s flat EPS over the last three years was below its 6.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Etsy’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 6.9× forward EV-to-EBITDA (or $43.06 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Etsy

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.