Looking back on gig economy stocks’ Q3 earnings, we examine this quarter’s best and worst performers, including Lyft (NASDAQ:LYFT) and its peers.

The iPhone changed the world, ushering in the era of the “always-on” internet and “on-demand” services - anything someone could want is just a few taps away. Likewise, the gig economy sprang up in a similar fashion, with a proliferation of tech-enabled freelance labor marketplaces, which work hand and hand with many on demand services. Individuals can now work on demand too. What began with tech-enabled platforms that aggregated riders and drivers has expanded over the past decade to include food delivery, groceries, and now even a plumber or graphic designer are all just a few taps away.

The 6 gig economy stocks we track reported a mixed Q3. As a group, revenues beat analysts’ consensus estimates by 1% while next quarter’s revenue guidance was 0.6% below.

While some gig economy stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 4.9% since the latest earnings results.

Lyft (NASDAQ:LYFT)

Founded by Logan Green and John Zimmer as a long-distance intercity carpooling company Zimride, Lyft (NASDAQ: LYFT) operates a ridesharing network in the US and Canada.

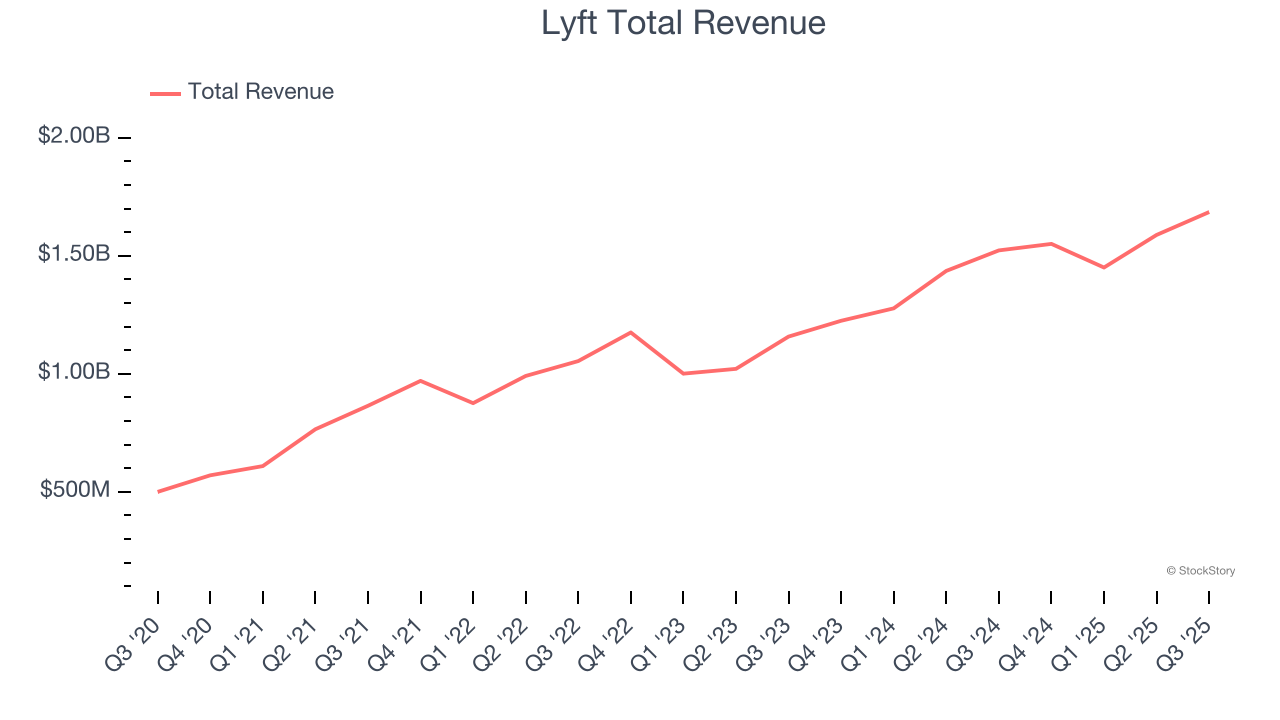

Lyft reported revenues of $1.69 billion, up 10.7% year on year. This print fell short of analysts’ expectations by 1.2%. Overall, it was a slower quarter for the company with a slight miss of analysts’ revenue estimates and a slight miss of analysts’ EBITDA estimates.

Interestingly, the stock is up 6.2% since reporting and currently trades at $21.35.

Is now the time to buy Lyft? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: Upwork (NASDAQ:UPWK)

Formed through the 2013 merger of Elance and oDesk, Upwork (NASDAQ:UPWK) is an online platform where businesses and independent professionals connect to get work done.

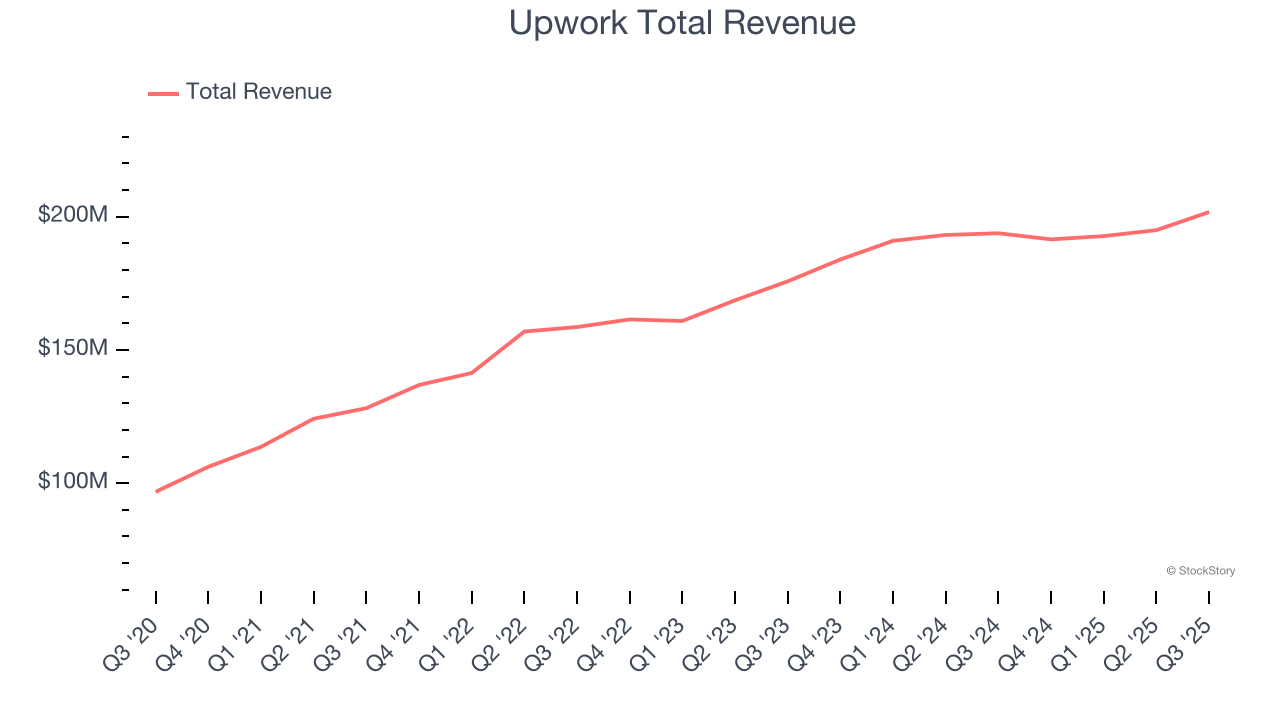

Upwork reported revenues of $201.7 million, up 4.1% year on year, outperforming analysts’ expectations by 4.3%. The business had a strong quarter with a solid beat of analysts’ EBITDA estimates and full-year EBITDA guidance exceeding analysts’ expectations.

Upwork delivered the biggest analyst estimates beat among its peers. On a dimmer note, the company reported 794,000 active customers, down 7.1% year on year. The market seems happy with the results as the stock is up 5.8% since reporting. It currently trades at $16.52.

Is now the time to buy Upwork? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Angi (NASDAQ:ANGI)

Created by IAC’s mergers of Angie’s List and HomeAdvisor, ANGI (NASDAQ: ANGI) operates the largest online marketplace for home services in the US.

Angi reported revenues of $265.6 million, down 10.5% year on year, falling short of analysts’ expectations by 1.2%. It was a slower quarter as it posted a decline in its requests and a significant miss of analysts’ number of service requests estimates.

Angi delivered the weakest performance against analyst estimates and slowest revenue growth in the group. The company reported 4.14 million service requests, down 7.7% year on year. As expected, the stock is down 10.4% since the results and currently trades at $11.53.

Read our full analysis of Angi’s results here.

Fiverr (NYSE:FVRR)

Based in Tel Aviv, Fiverr (NYSE:FVRR) operates a fixed price global freelance marketplace for digital services.

Fiverr reported revenues of $107.9 million, up 8.3% year on year. This result was in line with analysts’ expectations. Taking a step back, it was a mixed quarter as it also recorded an impressive beat of analysts’ EBITDA estimates but a decline in its buyers.

Fiverr pulled off the highest full-year guidance raise among its peers. The company reported 3.3 million active buyers, down 12.6% year on year. The stock is down 6.3% since reporting and currently trades at $20.25.

Read our full, actionable report on Fiverr here, it’s free for active Edge members.

Uber (NYSE:UBER)

Notoriously funded with $7.7 billion from the Softbank Vision Fund, Uber (NYSE:UBER) operates a platform of on-demand services such as ride-hailing, food delivery, and freight.

Uber reported revenues of $13.47 billion, up 20.4% year on year. This number surpassed analysts’ expectations by 1.5%. Aside from that, it was a satisfactory quarter as it also produced strong growth in its users but a slight miss of analysts’ EBITDA estimates.

The company reported 189 million users, up 17.4% year on year. The stock is down 7.5% since reporting and currently trades at $92.35.

Read our full, actionable report on Uber here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.