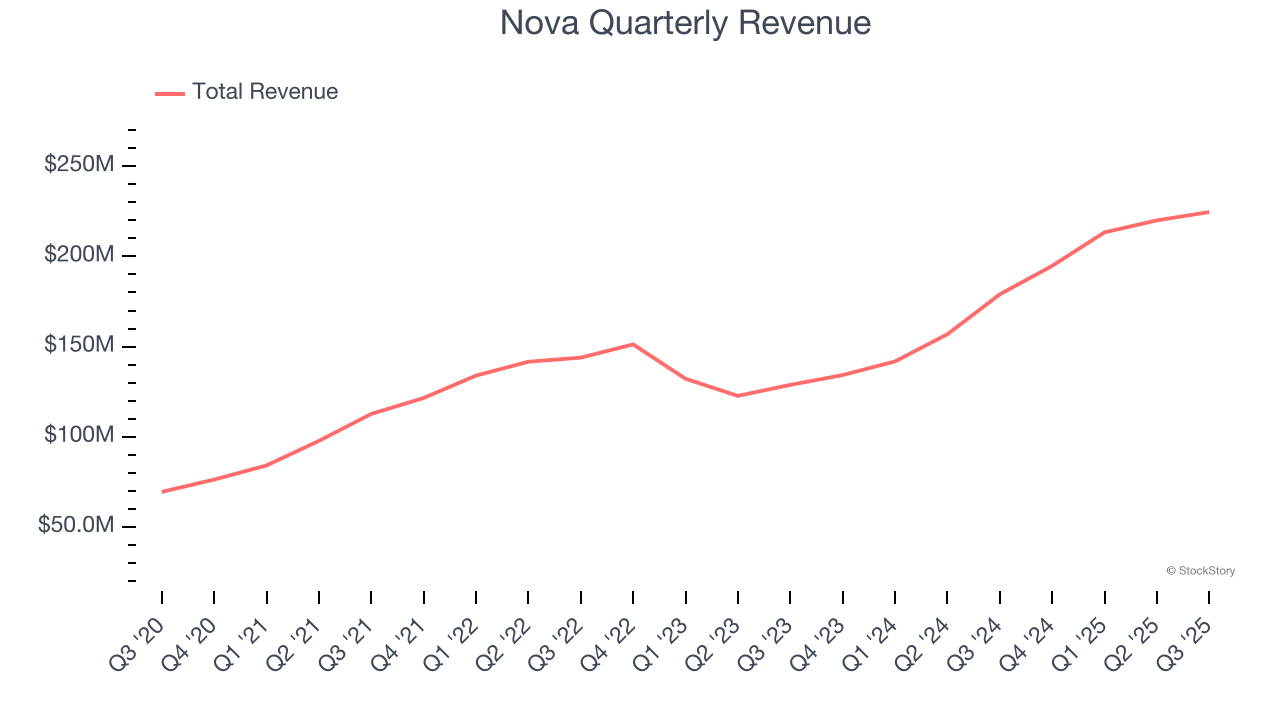

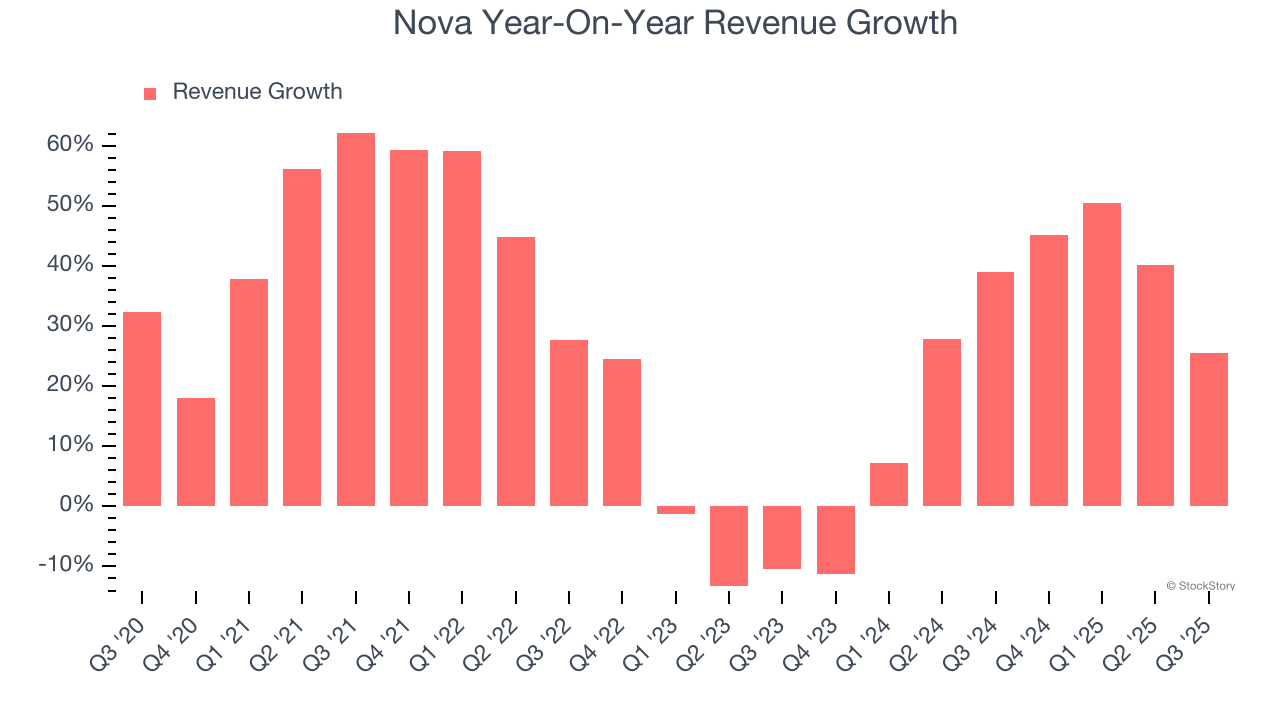

Semiconductor quality control company Nova (NASDAQ:NVMI) announced better-than-expected revenue in Q3 CY2025, with sales up 25.5% year on year to $224.6 million. Guidance for next quarter’s revenue was optimistic at $220 million at the midpoint, 2.4% above analysts’ estimates. Its non-GAAP profit of $2.16 per share was in line with analysts’ consensus estimates.

Is now the time to buy Nova? Find out by accessing our full research report, it’s free for active Edge members.

Nova (NVMI) Q3 CY2025 Highlights:

- Revenue: $224.6 million vs analyst estimates of $221.2 million (25.5% year-on-year growth, 1.5% beat)

- Adjusted EPS: $2.16 vs analyst estimates of $2.15 (in line)

- Adjusted Operating Income: $72.85 million vs analyst estimates of $72.98 million (32.4% margin, in line)

- Revenue Guidance for Q4 CY2025 is $220 million at the midpoint, above analyst estimates of $214.9 million

- Adjusted EPS guidance for Q4 CY2025 is $2.11 at the midpoint, above analyst estimates of $2.09

- Operating Margin: 28.4%, in line with the same quarter last year

- Free Cash Flow Margin: 29.8%, up from 24.1% in the same quarter last year

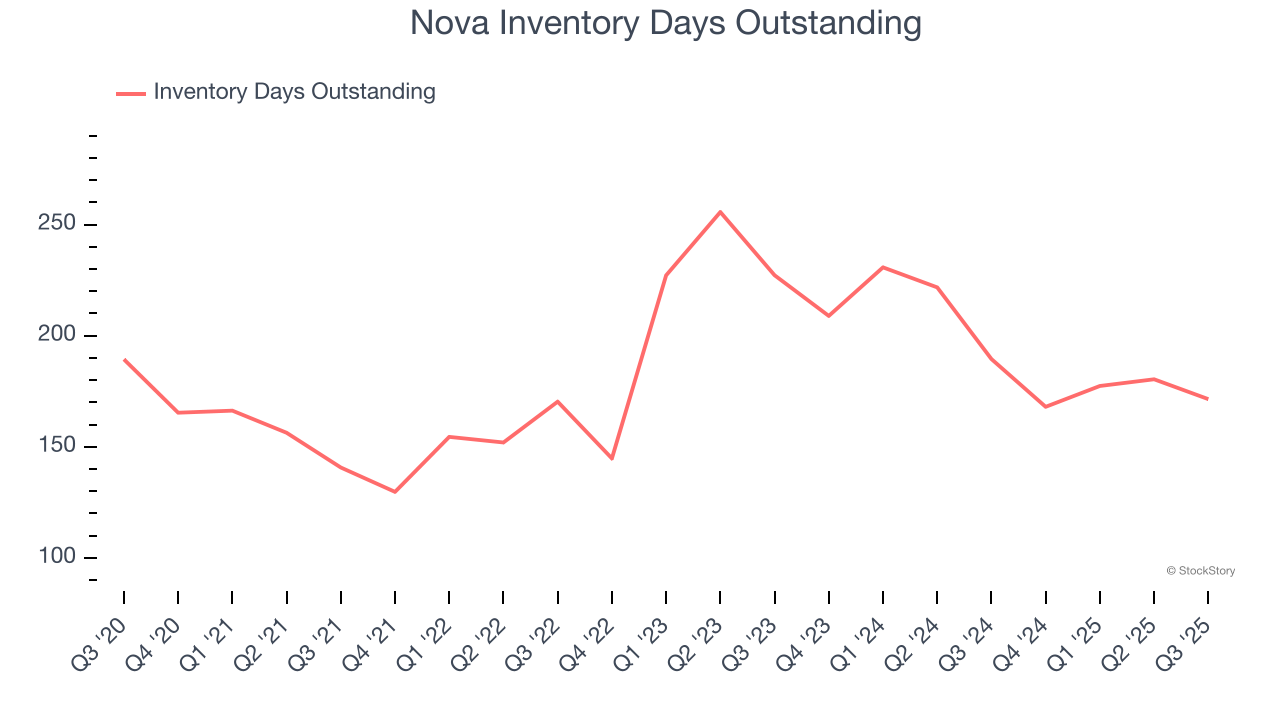

- Inventory Days Outstanding: 171, down from 180 in the previous quarter

- Market Capitalization: $10.15 billion

Management Comments "Nova achieved record third-quarter results, with the highest ever sales in memory and advanced logic, driven by strong demand for our advanced metrology solutions in leading nodes and advanced packaging," said Gaby Waisman, President and CEO.

Company Overview

Headquartered in Israel, Nova (NASDAQ:NVMI) is a provider of quality control systems used in semiconductor manufacturing.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Nova’s 27% annualized revenue growth over the last five years was incredible. Its growth surpassed the average semiconductor company and shows its offerings resonate with customers, a great starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Nova’s annualized revenue growth of 26.3% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Nova reported robust year-on-year revenue growth of 25.5%, and its $224.6 million of revenue topped Wall Street estimates by 1.5%. Beyond the beat, this marks 7 straight quarters of growth, showing that the current upcycle has had a good run - a typical upcycle usually lasts 8-10 quarters. Company management is currently guiding for a 13% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Nova’s DIO came in at 171, which is 10 days below its five-year average. At the moment, these numbers show no indication of an excessive inventory buildup.

Key Takeaways from Nova’s Q3 Results

A highlight during the quarter was Nova’s improvement in inventory levels. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 8.6% to $312 immediately after reporting.

So do we think Nova is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.